TINY HOUSE INSURANCE.

Welcome to tinyhouseinsurance.info where you can get a quote for all things tiny house related!

Featured Video

Why Tiny House Insurance Policies Are Being Canceled

Many tiny house owners assume that once a policy is issued, they are protected for the long haul. In reality, carriers are canceling and non-renewing more tiny house policies because custom builds do not fit cleanly into traditional home, RV, or manufactured-home categories.

Insurance companies want predictable risk. Tiny homes are rarely one-size-fits-all.

Michael from MAC Insurance explains what can trigger cancellations, what happens after a claim is reviewed, and why generic coverage can leave major gaps.

Custom builds create gray areasDifferent materials, certifications, and usage can make traditional policies a poor fit.

Claims receive closer scrutinyAn adjuster may discover details that do not match the policy originally written.

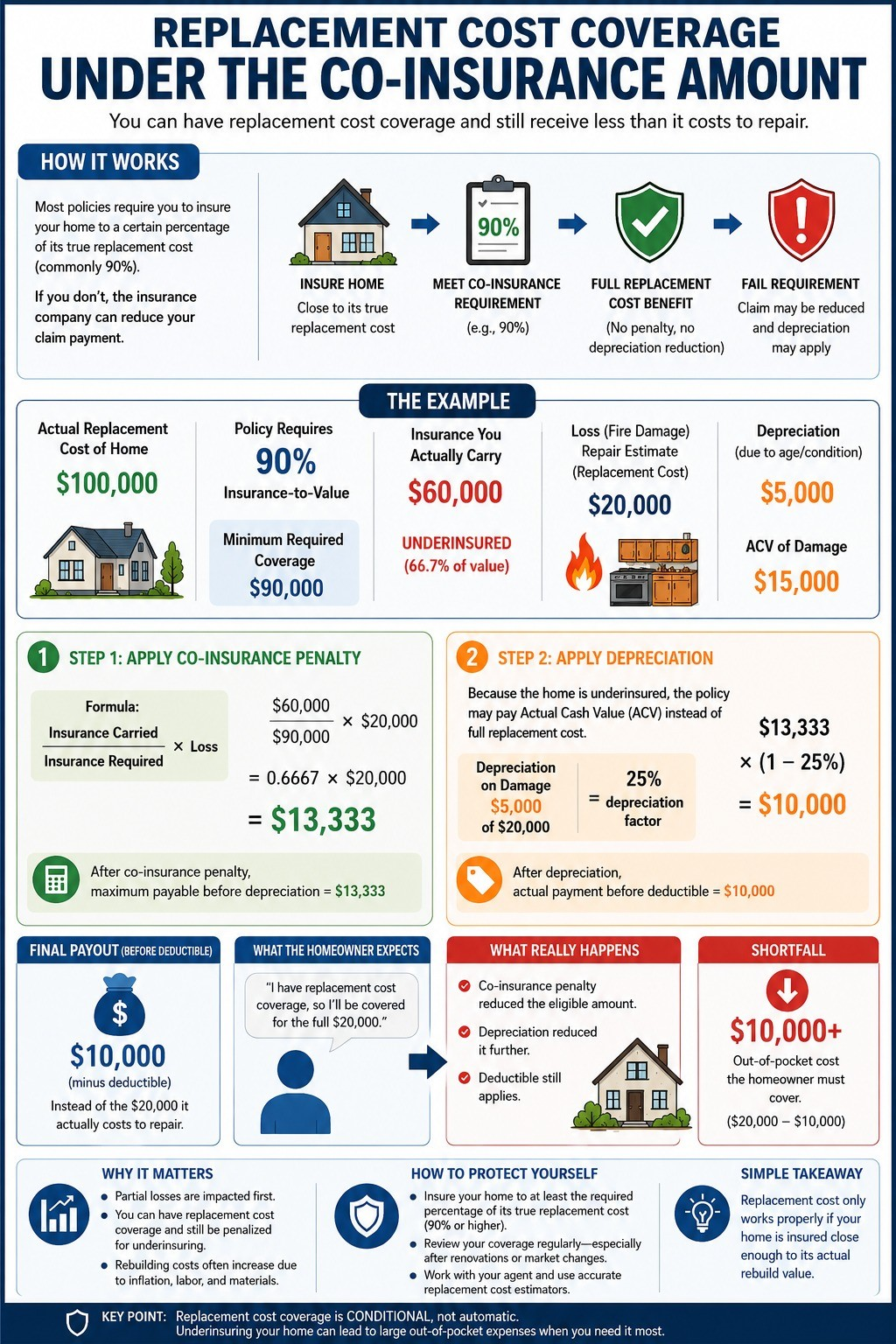

Replacement Cost & Co-InsuranceSee how replacement cost coverage worksClick to view the full guide explaining insurance-to-value, co-insurance penalties, depreciation, and why the insured amount matters.For tiny homes, the right coverage amount should reflect the real cost to repair or rebuild custom materials, appliances, labor, and attached features.Insure close to rebuild costReplacement cost works best when the insured value is close to the real cost to rebuild.Avoid underinsurance gapsIf the home is insured too low, claim payments may be reduced after a loss.Review the detailsDIY builds, decks, solar, sheds, and upgrades can all affect the amount needed.View full guide

Replacement Cost & Co-InsuranceSee how replacement cost coverage worksClick to view the full guide explaining insurance-to-value, co-insurance penalties, depreciation, and why the insured amount matters.For tiny homes, the right coverage amount should reflect the real cost to repair or rebuild custom materials, appliances, labor, and attached features.Insure close to rebuild costReplacement cost works best when the insured value is close to the real cost to rebuild.Avoid underinsurance gapsIf the home is insured too low, claim payments may be reduced after a loss.Review the detailsDIY builds, decks, solar, sheds, and upgrades can all affect the amount needed.View full guide What Sets MAC Insurance Apart

MAC Insurance, Inc. understands that tiny homes do not always fit neatly into a standard homeowners policy or a basic RV policy. Our tiny house insurance approach is built around the details that make these homes unique: how they were built, where they are placed, whether they move, and how they are used.

- Tiny house focusedOptions for DIY builds, professionally built homes, tiny homes on wheels, container homes, skoolies, yurts, cabins, and other unique small structures.

- Coverage that fits real lifePolicies can address trip endorsements, theft of the entire tiny home, liability, contents, and detached structures like decks, sheds, and solar panels.

- Niche guidanceMAC Insurance works with tiny house owners across more than 40 states and has built relationships throughout the tiny house community.

Coverage A Dwelling

This is the value used for the replacement of your tiny house if it were to get damaged. We insure as low as $25,000 to as much as $150,000.

Coverage B Other Structures

This is for your solar panels, built on decks, sheds, and other property structures that are not part of the tiny house.

Coverage C Contents

All personal belongings inside your house. If you were to turn your tiny upside down and shake it, whatever falls out would be part of your personal property.

Theft of Contents

We can also offer up to $3,000 in theft coverage for your belongings.

Trip Endorsement

If you're the type of person who travels with your home or needs to move it from an old location to a new location, we can make sure you are always covered on the go.

Theft of Tiny Home

If you are worried about your tiny house being stolen then you need this! 100% Coverage A replacement cost of the tiny house in cases of theft.

Tiny House/Yurt Questionnaire

If you are interested in a quote for your tiny house feel free to fill out the form below or contact us through our contact page.

We've gone ahead and answered many frequently asked questions below to help give a better understanding on what we do and what we can provide.

Tiny House/Yurt Questionnaire

Ready to tell us about your tiny home? Open the secure questionnaire when you are ready and a MAC Insurance specialist will review the details.

Google Reviews

TESTIMONIALS

Tiny house coverage help

Ready for a tiny house insurance quote?

Tell MAC Insurance about your build, location, and how you use your tiny home. A specialist will help you understand the right next step before you choose coverage.

- Stationary or mobile tiny homes

- Yurts, skoolies, cabins, and custom builds

- Coverage guidance by use and location